The Very Convenient Tesla 2026 Q1 Earnings Report

Tesla beat EPS. Net income up year-over-year. Free cash flow positive. The timing couldn't be better. Literally.

Disclaimer: all speculation and speculation only. Fun to read for fun. Not to be taken as financial advice or anything serious.

Yesterday, Tesla reported Q1 2026 earnings. Following are from CNBC, if you want to get the high level:

Here’s how the company did, compared with estimates from analysts polled by LSEG:

Earnings per share: 41 cents adjusted vs. 37 cents expected

Revenue: $22.39 billion vs. $22.64 billion expected

Tesla’s stock has underperformed all of its megacap peers so far this year, dropping 14% as of Wednesday’s close. The company’s core automotive business continues to struggle against competitors across the globe like China’s BYD and Xiaomi.

Yesterday I wrote about SpaceX buying Cursor. Let's just say, with that EPS number, it could be a rolling thunder approach (A marketing term in the valley basically saying one release good news after good news, instead of releasing them all at the same time). Except it wasn't.

Not only they didn't wait, it almost feel like the Cursor announcement is a distraction setup. Let me explain why I feel this way.

And, If you want to read more, I even have a piece that talks about Tesla vs. BYD, and why Tesla needs to make sense till SpaceX IPO.

So maybe we can speculate, that on Musk’s climbing to next success, Tesla is being moved from strategic to transactional. Before SpaceX goes public, the incentive to maintain Tesla’s market cap narrative maybe structural. When SpaceX goes public, we might be able to have a more clear picture.

The bottom line is simple:

Tesla is a company whose past innovation is being priced as future dominance. The gap between those two things is where the risk lives.

The Headline Mirage

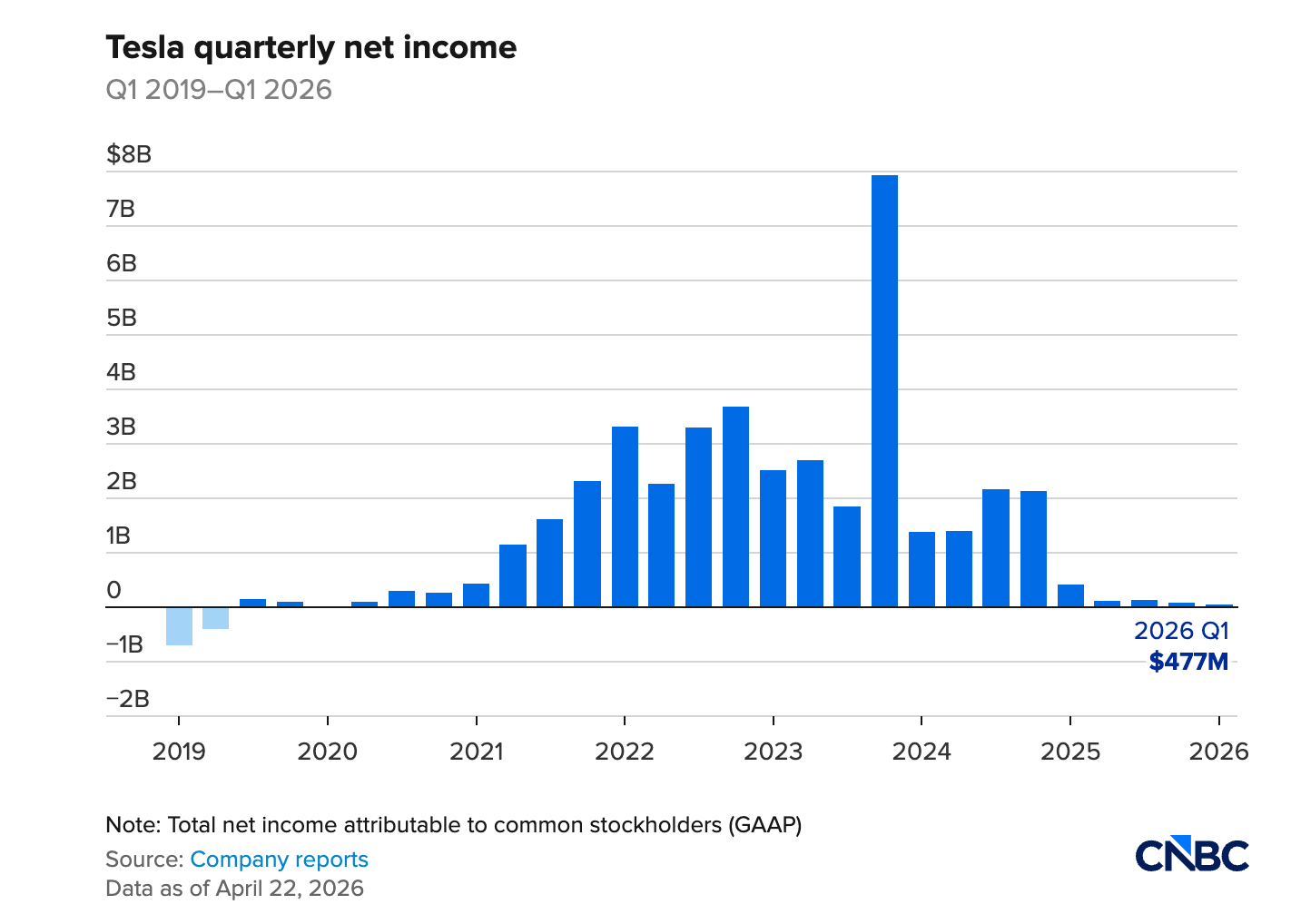

$477 million net income is surely a beat, and a significant year-over-year improvement. Numbers don't lie. But they can be coached to perform circus acts.

Let's just quickly check Tesla's (complete) net income chart.

A company in genuine recovery would let the numbers speak whenever they're ready. They'd give you the complete screenshot, if they believe investors would be impressed.

How To Make $477 Million Out of Thin Air

There are three ingredients in this quarter's profit. None of them will be available next quarter.

Ingredient One: The One-Time Tariff Rebate

CFO Vaibhav Taneja disclosed on the earnings call that Q1 benefited from approximately $250 million in one-time tariff-related benefits. This is listed in the shareholder letter under "increase in automotive one-time benefits related to warranty and tariffs." It is the number one driver of operating income improvement this quarter.

$477 million minus $250 million is $227 million.

This benefit will not repeat. Tesla did not earn this $250 million by selling more cars or cutting costs. They found it in an old coat pocket. The coat is now empty.

Ingredient Two: Borrowing Time from the Supply Chain

Tesla's days payable outstanding, the number of days it takes them to pay their suppliers, jumped from 61 days in Q4 2025 to 71 days in Q1 2026.

Ten extra days doesn't sound like much. It translates to accounts payable increasing by $1.325 billion in a single quarter, from $13.37 billion to $14.70 billion. Tesla is effectively using its suppliers as a zero-interest credit line. The operating cash flow headline of $3.94 billion, up 83% year-over-year, looks extraordinary. The accounts payable increase alone accounts for a meaningful portion of that improvement.

This is a very old trick. It is also not repeatable indefinitely. Suppliers eventually notice.

Ingredient Three: R&D Contribution

This one I want to show you rather than tell you.

In Q3 2025, Tesla's R&D expense was $1.15 billion. In Q4 2025, it was $1.20 billion. In Q1 2026, it dropped to $0.98 billion.

At the same time, intangible assets on the balance sheet jumped 74% in a single quarter, from $815 million to $1.42 billion. A $600 million increase.

R&D expense goes down. Intangible assets go up. By a suspicious magnitude, in the same quarter. Now, I'm not an accountant. You can draw your own conclusions about where the R&D went.

What I will say is this: if you add the $220 million reduction in expensed R&D back to the cost base, the profit number gets thinner. Add that to the $250 million in one-time tariff benefits, and you are looking at a business that, in its core recurring operations, barely broke even.

The Ghost in the Parking Lot

Tesla ended Q1 with 50,363 more vehicles built than delivered. Days of supply jumped from 15 to 27. Inventory on the balance sheet increased by $2 billion in a single quarter, from $12.39 billion to $14.43 billion.

These vehicles are sitting somewhere, waiting for buyers who have not yet arrived. Every day they sit there, they're worth a little less, and they pay for the storage.

The conventional explanation is that Tesla is building ahead of demand. The less charitable explanation is that building less can be costly.

This is actually a real phenomenon in capital-intensive manufacturing. Factories always carry enormous fixed costs. Depreciation, lease obligations, the labor that remains after all the layoffs. When you try to build less, those costs don't drop. They just get allocated across fewer vehicles, and the per-unit cost explodes, and the gross margin that everyone is celebrating disappears.

So you keep building, even if cars are already building up on parking lot, the 50,363 of them.

There is a word Elon Musk used to love when he was disrupting the auto industry. Don't build anything until a customer has asked for it. Eliminate waste. Overproduction is the original sin.

The Lean Manufacturing story left the building sometime in the last twelve months. Nobody announced its departure.

The Most Convenient Quarter

Here is the CapEx math.

Full year 2026 CapEx guidance? $25 billion. This is up from the "over $20 billion" guidance issued just three months ago at the Q4 2025 call. Yet, Q1 2026 capital expenditures was $2.49 billion. Not $5 billion, or $6.25 billion.

Musk didn't just delay spending; he held his breath. To meet the $25B guidance, Tesla must exhale $7.5B per quarter starting next Monday. Q1's free cash flow isn't a recovery; it's a temporary vacuum created to make the SpaceX IPO roadshow look breathable.

Q1 free cash flow: $1.44 billion. Positive. Looks good in a screenshot. Q2, Q3, Q4 free cash flow: CFO Taneja confirmed on the call that free cash flow will be negative for the remainder of the year.

Now the timing is interesting. The last quarterly report from Tesla before the planned SpaceX IPO just happened, and produced a positive free cash flow and positive net income. For investors who will decide whether to buy into the SpaceX IPO, this will be the last piece of recent Tesla financial data available to them.

Q2 will have a very different story, but that's after the IPO.

The Leviathan, Revisited

In 2017, MG Siegler wrote a piece called The Leviathan. Ohh I like it!

His argument was simple: Tesla is not a car company, not a tech company either. It is in its own category, a mythical creature operating in its own dimension, by its own rules, beyond the reach of conventional analysis.

That's precisely what we've seen since.

The audacity of the mission. The narratives that kept changing, and somehow kept working. The ability to survive what would have killed any other company ten times over. The short sellers who bet against Tesla includes Danny Moses and Bill Gates. They probably would get richer if they were betting against another company, but this is Tesla.

I think about that piece when I write this article. The Leviathan is still here. It is still enormous. It is still operating by rules that normal companies don't get to use. But even mythical creatures have to file quarterly reports.

And some quarterly reports just reveal how vulnerable they are.

The Valley Loves Him

Here is what I actually think.

A big portion of Silicon Valley's net worth is downstream of Elon Musk succeeding. Half of the valley will be on food stamp if SpaceX IPO fails.

I genuinely hope he pulls it off. The robots. The autonomy. The chip fab. The moon. The mars. The vision is extraordinary even if the Tesla quarterly numbers are not.

The Leviathan isn't bound by the laws of the ocean, but it is bound by the laws of physics and liquidity. Musk is betting that his vision can outrun his debt. In June, we’ll see if the monster can fly, or if it’s just a very expensive submarine.

For now, it's just parked next to 50,000 unsold cars, waiting for Q2.