Tesla’s Most Expensive Illusion

Everyone has an explanation for what’s happening to Tesla. Most of them are incomplete.

In 2025, Tesla’s global deliveries dropped 8.6% to 1.636 million vehicles,and revenue fell 3%. It’s the first annual decline in its history. The net income collapsed 46.5%.

The explanation we hear most: Elon Musk alienated Tesla’s core buyers. EV buyers skew left. Musk went right. Buyers walked.

Where the Explanation Breaks Down

Sure, it might have something to do with political views.

In 2022, Tesla held approximately 75% of the US EV market. By 2025, that had fallen to 46% — and touched 38% in August, more than halved in three years. The political story feels right in US. After all, we’ve all seen this somewhere, one someone’s Teslas.

Yet if this were purely a political problem, it would show up unevenly across the world. Strongest in politically polarized markets, weaker elsewhere. We are likely to see drops in left-leaning countries, numbers go up in right-leaning countries. But that don’t explain broader EU or Norway, or Czechia.

Europe: EV market grew, and Tesla didn’t:

The broader European EV market grew rapidly. Battery-electric cars reached 17.4% of EU registrations in 2025, up from 13.6% in 2024. Yet January 2026 marked Tesla’s 13th consecutive month of year-over-year decline. Every single European market fell in 2025, including right-leaning Czechia, except the left-leaning Norway.

China has the most intriguing number of all:

2025 sees Tesla’s first annual decline ever in China. Tesla operates Gigafactory Shanghai with full local manufacturing advantages. There is no import tariffs, no supply chain penalties, and American political noise was registered differently. Elon was and still is loved in China. The broader Chinese EV market kept growing. Tesla shrank inside it, quietly.

Politics doesn’t explain lots of countries.

Something else is happening.

Case Study I: The Product Comparison with BYD

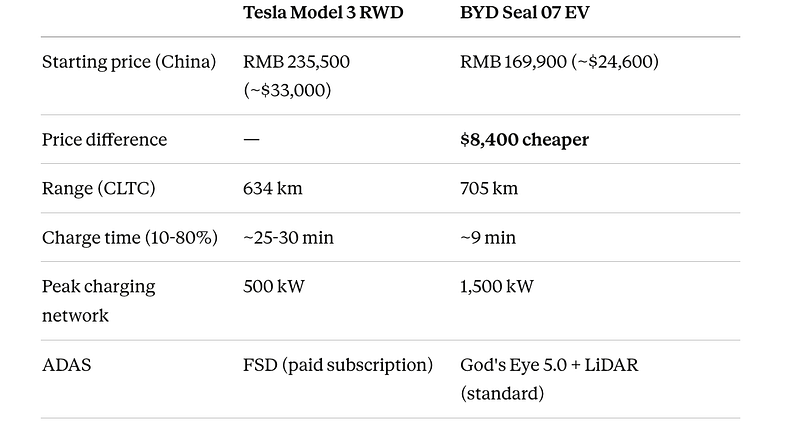

Let’s start with some number comparison between Tesla Model 3 and BYD Seal 07 EV. It worth noting that BYD launched the Seal specifically as a Model 3 competitor. It targets the same segment, same price bracket, for the same target buyers.

The BYD entry model is $8,400 cheaper. It goes 71 km further on a single charge, and charges almost three times faster. And the advanced driver assistance system that Tesla charges a monthly subscription for? Standard on every BYD Seal 07, included in the price.

What’s also included in the price is the standard LiDAR, something that provides much better sensing of road conditions, especially in bad weather or at night. When Musk called LiDAR a fool’s errand, he was right about the price. He just didn’t account for what Chinese manufacturing would do to that price.

There is one more thing the BYD can do that the Tesla cannot. BYD’s Seal family supports V2L (Vehicle-to-Load), meaning one can plug the car into home and run appliances directly from the battery. During a power outage, a wildfire evacuation, or a storm, the car becomes a 69 kWh backup generator. Tesla’s Model 3 does not support V2L. If we want that capability with a Tesla, we’ll need a Powerwall that starts at around $11,500, installed separately.

Some people buy a car. Some people buy energy infrastructure. BYD is selling both at $8,400 less than Tesla model 3.

No wonder BYD sold 4.27 million vehicles globally in 2025. The gap is widening.

That’s not purely because of politics.

Tesla’s Greatest Contribution

Let’s be honest. Tesla proved EVs could scale. It pioneered vertical integration at gigafactory scale. Without Tesla, the global EV transition would be years behind. That’s the zero to one contribution and it is brilliant.

Today, Tesla’s advantage wasn’t lost. It was absorbed.

The Gigafactory model is now the industry standard. BYD has more manufacturing capacity. CATL built its own version. Volkswagen, Stellantis, Hyundai — all retooled around lessons Tesla taught them.

The pioneer blazed the trail. Then everyone walked it. And some walked faster.

Battery : Where the Innovation Happens

Battery defines the EV. Everything else is just the transport. Once considered ahead of the curve, Tesla is now measurably behind what matters the most.

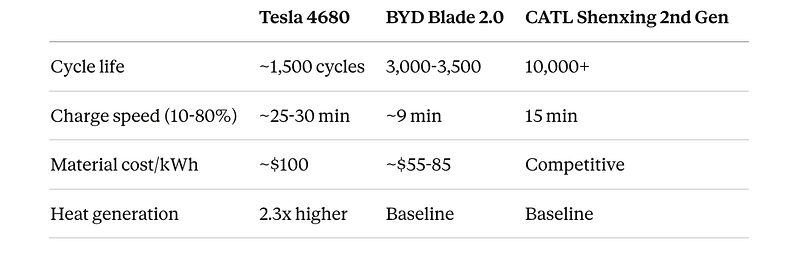

CATL’s 10,000 cycle claim means 15+ years of projected battery life. Tesla’s 4680 loses 15% capacity after 1,500 cycles. For mass markets where buyer would finance the car, battery longevity is resale value. That mathematics is now very visible in the used Tesla market.

Tesla is not investing enough in the one area that defines the product. If we look closer, we’ll find that Tesla’s own Model 3 Standard Range in China runs on CATL batteries. Tesla is outsourcing to the competition it is losing to.

The AI Pivot and the Robotaxi — Narrative Running Ahead of Reality

Tesla now describes itself as a “physical AI company”, not a pure EV maker.

Its FSD subscriptions more than doubled in 2025, driven by its aggressive incentives. Robotaxi launched in Austin, and Optimus robots is now in production. The narrative is consistent, Tesla is an AI company.

That’s extremely smart. Tesla cannot justify a $1.2 trillion market cap as a declining EV company. But as an AI platform? The math works, on paper. The pivot accelerated precisely as EV sales started declining. That timing is wise.

The product and the operation behind it, however, may not be ready yet.

Case Study II: Robotaxi vs. Waymo

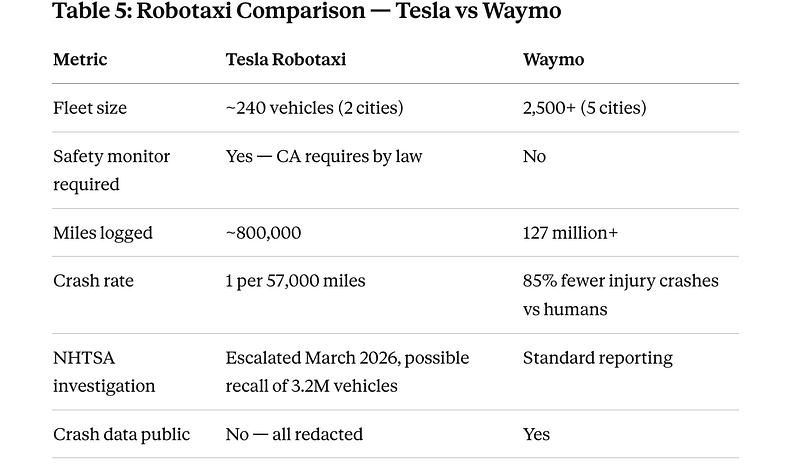

Tesla’s robotaxi fleet now has approximately 89vehicles, and 168 in San Francisco. Every vehicle carries a trained safety monitor, as required by law.

In case we wonder how they are doing in driving compare with human drivers, the fully driverless Waymo reduces injury crashes by 85% compared to humans.

However, Tesla’s robotaxi crashes approximately 9 times more often than the average human driver, based on police report. That is while a safety monitor person is present. In March 2026, NHTSA escalated its FSD investigation.

So, the Robotaxi story is still too early and too slow. If robotaxi is the future, the data suggests Waymo is a better bet.

The $56 Billion Mechanism

What follows is a informed speculation. Informed, but still just speculation.

In December 2025, the Delaware Supreme Court restored Musk’s compensation package — approximately $56 billion in Tesla stock. The financial press treats this as the trophy. Many assume getting that $56 billion is Musk’s end goal.

It may be the infrastructure.

Musk runs Tesla, SpaceX, xAI, X, Neuralink, The Boring Company, and DOGE simultaneously. In January 2026, Tesla invested $2 billion in xAI. Weeks later SpaceX acquired xAI at a $1.25 trillion valuation. Tesla shareholders are suing Musk for breach of fiduciary duty. Musk then admitted xAI “was not built right first time around.”

What does $56 billion in Tesla stock do for someone whose paper wealth has since crossed $1 trillion?

It keeps the narrative alive. It keeps the market cap inflated. And an inflated market cap is always the collateral: for the Twitter/X acquisition financing, for xAI, for the SpaceX-xAI IPO targeting $50 billion, for whatever comes next.

The compensation package is valued in Tesla stock. The higher the stock, the bigger the prize. The incentive to maintain the narrative couldn’t be more direct.

Tesla may be functioning as a cash cow and collateral engine for something much larger being assembled elsewhere.

The $56 billion may not be the prize. It may be the price of keeping everyone looking the other way.

So Where Does This Leave Us?

Key takeaway: Tesla is weaker than it appears, and it is not only because of politics.

Technologically, it is losing the battery war. The manufacturing advantage it built was real. But that is absorbed into all its competitors.

At this point, it is optimizing for market cap and software margin, not product competitiveness. The AI narrative is running years ahead of the product.

So maybe we can speculate, that on Musk’s climbing to next success, Tesla is being moved from strategic to transactional. Before SpaceX goes public, the incentive to maintain Tesla’s market cap narrative maybe structural. When SpaceX goes public, we might be able to have a more clear picture.

The bottom line is simple:

Tesla is a company whose past innovation is being priced as future dominance. The gap between those two things is where the risk lives.

As your fellow Tesla driver, who’s on her second tesla even though she knows Musk was crazy when the decision was mode, I’d say drive carefully. Stay awake at the wheel. If you use FSD, I wrote about why in November 2025 . The Robotaxi data since then has only confirmed it.

If you are a heavy reader and a stock trader who has nothing better to do for 5 min, I'd also suggest you read this piece: The number on the balance sheet was always clean. The life underneath it wasn't.

And subscribe if you want notification for the next piece: Why this is bigger than Tesla.

Sources

Deliveries & Financial Performance

Tesla Q4/FY2025 Shareholder Update — global deliveries, revenue, net income, FSD subscription growth, robotaxi launch

Tesla Q4/FY2025 Annual Report — “physical AI company” framing, Optimus production

North America Market Share

CleanTechnica, Feb 2026 — Tesla US EV market share 46% in 2025, down from 49% in 2024

Reuters / GCBC — Tesla US EV market share fell below 40% in August 2025, lowest since 2017

CarEdge — Tesla held ~75% US EV market share in 2022

Europe

ACEA (European Automobile Manufacturers Association) — January 2026 registrations; BEV market share 17.4% in 2025 vs 13.6% in 2024

CnEVPost, Jan 2026 — BYD European registrations 187,657 in 2025 (+268.6%); Tesla 238,656 (-26.9%)

Electrek, Jan 2026 — Tesla 13th consecutive month of year-over-year decline in Europe

Automotive World, Jan 2026 — Tesla European sales by country: Germany -48.4%, Sweden -66.9%, Belgium -53.1%

China

China Passenger Car Association / CNBC — Tesla China wholesale deliveries Jan–Nov 2025

CnEVPost, Jan 2026 — BYD global BEV sales 2.26M in 2025, surpassing Tesla’s 1.636M for first time

CNBC, Jan 2026 — Xiaomi 410,000 deliveries in 2025; Xpeng 429,445 (+126%)

Product Comparison

Tesla China configurator — Model 3 pricing

Reuters / CarNewsChina, Mar 2026 — BYD Seal 07 EV launch pricing (~169,900–189,900 yuan)

BYD launch event, Mar 2026 — Blade Battery 2.0 charging specs

Battery Technology

Gorsch et al., Cell Reports Physical Science, Mar 2025 — peer-reviewed teardown of Tesla 4680 vs BYD Blade: cycle life, heat generation, material cost (~€10/kWh BYD advantage)

CATL Tech Day 2025 — Shenxing 2nd gen specs, 10,000+ cycle claim

AI Pivot & Robotaxi

Tesla Q4/FY2025 Update — FSD subscriptions more than doubled; robotaxi Austin launch June 2025

NHTSA Standing General Order database — 15 Tesla robotaxi crashes in Austin through Mar 2026; one crash per ~57,000 miles

Electrek, Feb–Mar 2026 — crash rate analysis vs human average (500,000 miles); Waymo 127M driverless miles

Reuters / NHTSA — FSD investigation escalated March 2026

The $56 Billion

Reuters, Dec 2025 — Delaware Supreme Court restored Musk’s 2018 compensation package

Tesla SEC disclosures / Reuters — Tesla $2 billion xAI investment, Jan 2026

Electrek / CNBC, Feb 2026 — SpaceX acquired xAI at $1.25 trillion valuation

Fortune / Electrek, Mar 2026 — Musk admitted xAI “was not built right first time around”; 10 of 12 co-founders departed

Forbes Real Time Billionaires — Musk paper wealth ~$852 billion